The home buying process is an intricate maze full of both success stories and pitfalls. What's especially difficult is figuring out its financing part. When dealing with a mortgage, you couldn't be too complacent and not invest your time and negotiate properly for the best one that suits you. Moreover, making one mortgage mistake can be the difference between getting approved for your loan application or not.

Here are nine of the most common mortgage blunders that buyers make. Make sure you think about how you could avoid them for you to have a pleasant and meaningful home buying experience.

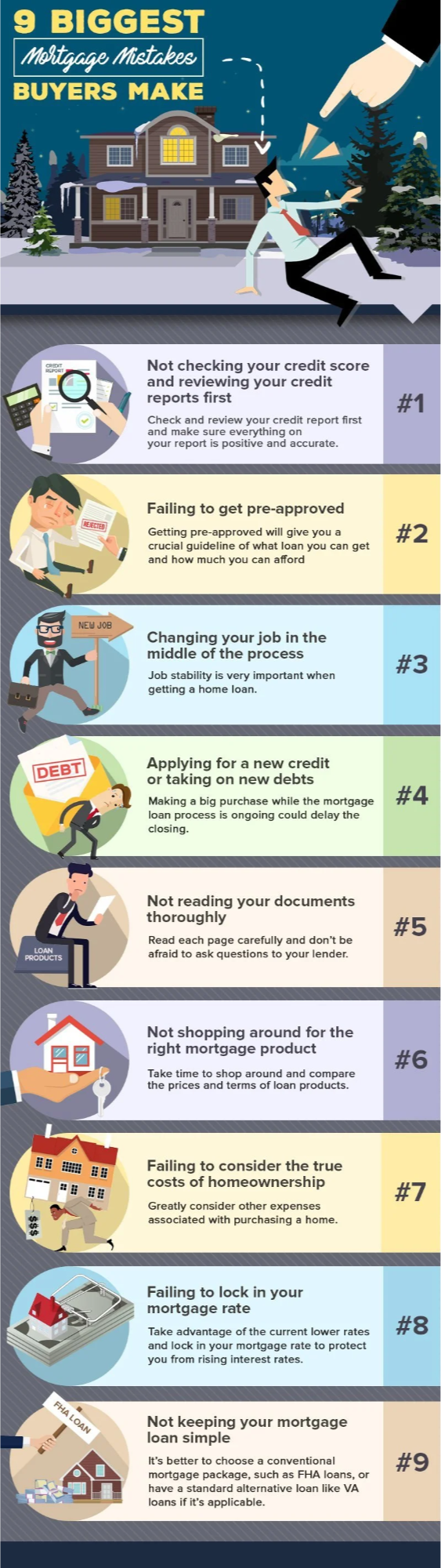

Mistake #1: Not checking your credit score and reviewing your credit reports first

Even before you consider buying your own home, your first homework is to check and review your credit and make sure everything in your report is accurate. Checking your credit report firsthand could help you avoid any issues further down the process.

Review all three of your credit reports from the main credit bureaus, and if there are errors or any inaccurate information in your report, take the necessary steps to dispute them immediately.

If your credit score isn't in its best shape, you can consider these helpful measures to improve it. Ensuring that everything on your credit report is positive and accurate is the first step for you to have a swift and smooth loan approval process.

Mistake #2: Failing to get pre-approved

Not getting pre-approved is the most common mortgage mistake home buyers make. There's also a big difference between getting a pre-qualification letter and getting a pre-approval.

More than getting pre-qualified, where you can get an idea of what home you can afford and what your monthly payment will be, getting a mortgage pre-approval is a notch better. Getting pre-approved will provide you with a crucial guideline of what loan you can get, how much you can afford, and can also give you an accurate estimate of how much the bank will lend you. The lender will verify your credit and employment which will help you avoid potential issues that could prevent you from getting your dream home.

Mistake #3: Changing your job in the middle of the process

One popular mistake when buying a home is changing jobs while you’re in the process of receiving a mortgage loan. Job stability is very important when getting a home loan because mortgage companies greatly take into consideration the borrower’s job history when approving or denying. Changing your job could complicate the process since the mortgage lender will need to reevaluate the stability of your position and your capability to pay off your debt. Even if you’re moving into a higher position, it is best to ask your employer if you could start after your closing date.

Mistake #4: Applying for a new credit or taking on new debts

Another big mistake home buyers make is taking on new debts or applying for new credit. Making a big purchase while the mortgage loan process is ongoing could delay the closing. It could also mess up the borrower’s debt-to-income ratio, which could result in being denied a mortgage. Applying for new credit can hurt your credit score and increase your debt load. So if you’re eyeing a new car or an enormous flat-screen TV, it is best to buy it when the loan is already funded and closed.

Mistake #5: Not reading your documents thoroughly

Before signing your loan documents, it would really help if you read each page carefully and not be afraid to ask questions to your lender if there’s something you’re not confident with. Some loan and mortgage terminologies can be very technical or confusing, but it wouldn’t hurt to put on your nerdy cap and review your documents thoroughly to know the terms and inclusions.

Mistake #6: Not shopping around for the right mortgage product

Just like how you’d take time to compare and review other products before buying them, devoting time to do “mortgage rate shopping” can save you thousands of dollars in fees and interests later on. Take time to shop around and compare the prices and terms of loan products. You may be surprised to know that sometimes, even the one with the lowest interest rates may not be the best offer. Lower rates may have steep fees and other terms that may prove to be not desirable at all.

Likewise, don’t get intimidated by the mortgage transaction itself. Compare good and bad recommendations and reviews. Shop around for the best possible terms applicable to you, and decide which type of mortgage best suits your situation and capability.

Mistake #7: Failing to consider the true costs of homeownership

What many first-time homebuyers fail to realize is that there are other expenses associated with purchasing a home aside from the mortgage payment itself. Once you open the door and step into homeownership, other costs associated with it will come rushing in. You have to pay for property taxes, homeowners’ insurance, and HOA fees if applicable. You also have to allocate a budget for other necessary purchases, potential repairs and maintenance, and other incidentals.

Mistake #8: Failing to lock in your mortgage rate

In completing a mortgage application, buyers also have to decide whether they’d like to float or lock their mortgage rate. Not locking in your mortgage rate is a big risk since interests are expected to rise every quarter of the year. The 2018 Mortgage Rate Forecast of the Mortgage Bankers Association suggests the first quarter will have a 4.3% interest rate and will rise to 4.8% by the last quarter. If you decide to buy a home, take advantage of the current lower rates and be sure to lock in your mortgage rate. Also, it is best to closely monitor the interest rates before and during the closing process.

Mistake #9: Not keeping your mortgage loan simple

Keeping your mortgage loan simple could be your best option if you want a less stressful process. Despite the many unique loan packages available out there, many of them come with complications and terms that may pose more restrictions. Some mortgage options even have superficial collections or charge-offs that could affect your credit score. It’s better to choose a conventional mortgage package, such as FHA loans, or have a standard alternative loan like VA loans if it’s applicable. Likewise, don’t be afraid to always consult with your top real estate agent about your financial needs and about the whole mortgage process.

FROM OUR BLOG

The Invisible Tier: Why Montclair Homes Sell $300K Over Their List Price

The Invisible Tier: Why Montclair Homes Sell $300K Over Their List Price Thirty-eight Montclair homes have closed between $1M and $1.5M this year — and most of them were never listed there. If your search filter starts at $1M, you're shopping a market you can't see. Rate & Market Pulse Freddie Mac's

What $1.7 Million Is Actually Doing in Bergen County

Northern New Jersey Real Estate Weekly What $1.7 Million Is Actually Doing in Bergen County A Northern New Jersey read on the county's busiest luxury tier While the headlines wait on the Fed, Northern New Jersey's $1.5–$2 million market has spent the entire year doing one quiet thing on repeat

The Market Moved Upstairs: Where Northern NJ Home Sales Are Growing in 2026

The market didn’t freeze — it moved up the price ladder. What that means across Northern NJ. The Market Moved Upstairs Across Northern NJ, the entry-level market is shrinking while the move-up tiers keep expanding — here’s what that means for your next move. Rate & Market Pulse The headline out of

About the Authors

Eric & Kathryn DeSilva are local North Jersey real estate advisors specializing in strategic pricing, digital marketing exposure, and data-driven negotiation. Based in Nutley, they serve Essex and Bergen County homeowners and buyers.

Thinking About Making a Move in 2026?

Whether you're buying or selling in Nutley or surrounding North Jersey towns, we help you move with strategy — not guesswork.

BUYER SERVICES

We're here to help you find the home of your dreams. With a team of experts guiding you every step of the way, our extensive knowledge and experience will ensure you have the best home buying experience possible.

SELLER SERVICES

We take the stress out of selling your home by providing a seamless experience from start to finish. Our team will put you in the best position to market your home and sell it for the highest possible price.